BOFIT Viikkokatsaus / BOFIT Weekly Review 2015/46

The value of goods imports in July-September fell about as fast as the value of exports. The contraction in imports was broad-based, with falling demand and the weak ruble affecting nearly all product groups and markets. Economic sanctions did not play a crucial role in the overall reduction in imports. Imports from EAEU countries, however, have been supported since late August by sharp depreciation of the Kazakhstan tenge and the Belarus ruble. In the largest product categories, the value of imports of machinery, equipment & transport equipment was down 40 % y-o-y, while imports of chemical products and foodstuffs each contracted by 30 %.

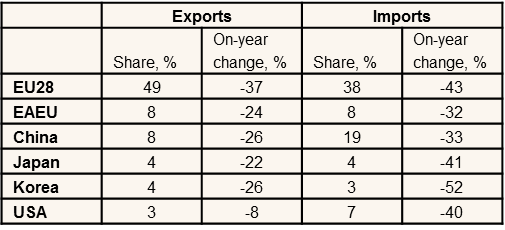

The value of Russian goods exports in the first nine months of the year amounted to about $260 billion, while goods imports were valued at roughly $140 billion. The structures of imports and exports in terms of countries and product groups have not changed significantly lately. Nearly half of exports consisted of crude oil and petroleum products. Natural gas accounted for about 15 % of exports, followed by metal and chemical products at about 10 %. Over 40 % of imports consisted of machinery, equipment & transport equipment, followed by nearly 20 % share of chemical products and nearly 15 % of foodstuffs. The EU as a whole was clearly Russia’s most important trading partner, while the single largest market in Russia’s foreign trade was China.

Russian foreign trade, January-September 2015

Source: Russian customs.