BOFIT Viikkokatsaus / BOFIT Weekly Review 2016/24

A significant barrier to inclusion of Chinese A-shares in the MSCI EM index appears to be repatriation limits for invested assets and pre-approval restrictions imposed by Chinese stock exchanges on releasing international investment products containing A-shares. The thorniest problem for investors seems to be the 20 % repatriation limit, i.e. only a fifth of previous year’s net value of QFII investments can be repatriated in a given month, which means it takes about five months to close out a position. MSCI EM index currently includes Chinese shares listed on the Hong Kong or US exchanges, and the shares have about 20 % weight in the index.

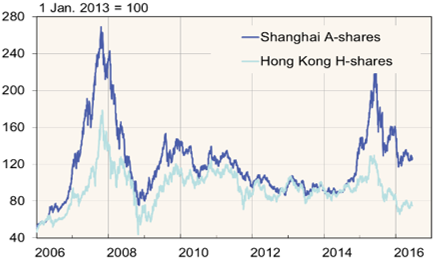

The fundamental barrier to access to Chinese stock markets is that international investors can only invest through special programmes with imposed quotas. As an example of this market access constraint, share prices for the same firm currently average about 35 % more on the Shanghai and Shenzhen exchanges than in Hong Kong. The linking of the Shenzhen and Hong Kong exchanges is set to begin shortly. Even if this improves access of international investors to the Chinese market, however, China’s hoped-for inflows of foreign capital and investor knowhow into its financial markets have remained meagre since the Shanghai-Hong Kong process began in late 2014.

A- and H-share prices on Shanghai and Hong Kong exchanges

Source: Macrobond.